News

Details of Tax Evasion by a Livestreaming Host with '6 Million Followers': Evading Taxes via a 'Hidden Ledger'

According to the official website of the State Taxation Administration, on July 10, 2026, tax authorities publicly released details of seven cases of tax evasion involving influencer online stores. Among them was a case of tax evasion by livestreaming host Xu Jingwan, investigated and handled in accordance with the law by the Third Inspection Bureau of the Hangzhou Municipal Taxation Bureau under the State Taxation Administration.

The Paper noted that Xu Jingwan is the influencer with the largest follower base among the livestreaming hosts exposed this time, with a combined following of over 6 million, and is also the host who evaded the most taxes—a typical case of "high traffic, low declaration."

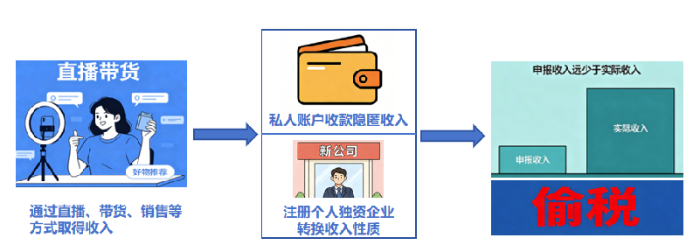

Investigations found that from 2021 to 2023, Xu Jingwan engaged in livestream commerce on online platforms and underpaid individual income tax, value-added tax, and other taxes totaling 3.1345 million yuan, by means such as concealing income through private-account receipts and converting the nature of her income.

In December 2025, the Third Inspection Bureau of the Hangzhou Municipal Taxation Bureau imposed a ruling requiring the recovery of tax payments, the levy of late fees, and a fine totaling 6.3196 million yuan. To date, all involved tax amounts, late fees, and fines have been fully recovered and turned over to the state treasury.

The Hangzhou Municipal Taxation Bureau disclosed the investigative process of this case.

Image source: Official website of the Zhejiang Provincial Tax Service, State Taxation Administration

According to the disclosure, the Third Inspection Bureau of the Hangzhou Municipal Taxation Bureau earlier identified, through big-data analysis, that livestreaming host Xu Jingwan conducted livestream sales across multiple platforms. Her accounts had a combined follower base of over 6 million and her livestream rooms were highly popular; the products displayed in her account storefronts were priced at several hundred yuan each, with hundreds of units sold per item—yet the individual income tax she declared and paid was minimal, wildly out of proportion to her sales traffic.

At the same time, tax authorities reviewed the tax filing data of the business entities associated with Xu Jingwan and found that the two online stores she was responsible for had reported zero taxes of every category since their establishment—inconsistent with the scale of sales shown in public information, raising suspicion of underreported income.

Based on the above red flags, the Third Inspection Bureau of the Hangzhou Municipal Taxation Bureau decided to open a formal investigation into Xu Jingwan in accordance with the law.

However, when first questioned by inspectors, Xu Jingwan claimed she had little knowledge of tax law and was unclear about how much income she had reported earlier. Regarding the suspicion of "zero declarations" by the two online stores, Xu stated that she was in a cooperative relationship with them—merely helping sell women's clothing and collecting advertising and promotion income—and was unaware of their tax filing matters.

Was the truth really as Xu Jingwan claimed? To get to the bottom of it, inspectors lawfully obtained and analyzed the sales data of Xu's livestream stores and the fund-flow records of multiple accounts under her name. Through transaction-by-transaction cross-comparison of the fund flows, inspectors found that although the legal representatives of the business entities bound to the two online stores were not Xu Jingwan, almost all of their sales revenue was cashed out to Xu's personal accounts.

Subsequently, through investigation, inspectors obtained a list of enterprises registered under Xu Jingwan's name. Among them, a sole proprietorship she had registered—Shanghai Wanda Business Consulting Center—caught their attention. After reviewing the center's account flows, inspectors found that since its establishment the enterprise had never recorded any expenses such as office rent or utilities, and had no affiliated personnel paying social insurance—all of which confirmed that the enterprise had never actually conducted business operations.

Records showed that the enterprise declared and paid taxes as business income for the period 2021–2022. After analyzing and comparing the memo information in the relevant account flows, inspectors discovered that the income it declared appeared on the surface to be Xu Jingwan's personal advertising revenue, but was in fact her personal labor remuneration—constituting an improper conversion of the nature of her income.

Meanwhile, inspectors found that service-fee income and rental income Xu Jingwan settled offline had not been declared or taxed in accordance with the law. At this point, a clearly traceable "map" of tax evasion was laid out before the inspectors.

After gathering substantial foundational evidence, inspectors lawfully summoned Xu Jingwan for an interview. After the inspectors presented the key evidence one by one and explained in detail the relevant tax laws and regulations and the consequences of violations, Xu Jingwan ultimately truthfully admitted the facts of her tax violations.